Angola – Revised Medium Term Development Plan – 2018-2022

December 17, 2020

Compared Analysis: Transfer Pricing in Angola, Mozambique and Portugal

December 22, 2020

On December 18th, 2020, the Argentine Official Gazette published Law No. 27.605, which creates a One-time Emergency, Extraordinary and Mandatory Contribution to be afforded by the following persons depending on the value of their assets by the time this Law becomes effective:

a) Resident Individuals and Undivided Estates, for their assets located in Argentina and abroad, valuated in line with the provisions of the Wealth Tax Law, as amended, regardless of the tax treatment provided by said Law, and with no minimum non-taxable amount.

Resident individuals with Argentine nationality but that are residents or domiciled in “non-cooperative jurisdictions” or “low tax jurisdictions or tax havens”, in terms of articles 19 and 20 of the Income Tax Law, as amended.

In this case, the taxable base shall be determined including contributions to trusts, funds, private foundations and similar structures, participation in entities with no tax personality, and direct or indirect participation in entities in existence by the time this Law becomes effective.

b) Foreign Individuals and Undivided Estates, but those located in non-cooperative and/or low tax jurisdictions, for their assets located in Argentina, valuated in line with the provisions of the Wealth Tax Law, as amended, regardless of the tax treatment provided by said Law, and with no minimum non-taxable amount.

The Law specifies that if the value of the total assets does not exceed AR$ 200,000,000, inclusively, the abovementioned persons shall be exempt from this Extraordinary and Mandatory Contribution.

Further, for purposes of residency rules, it remits to articles 116 – 123 of the Income Tax Law, as amended.

Resident Individuals, undivided estates, and single-owner entities that are co-owners, or hold, or have the right to use, dispose, or are custodians of assets belonging to foreign persons, must act as Substitute Responsible Parties of this Contribution.

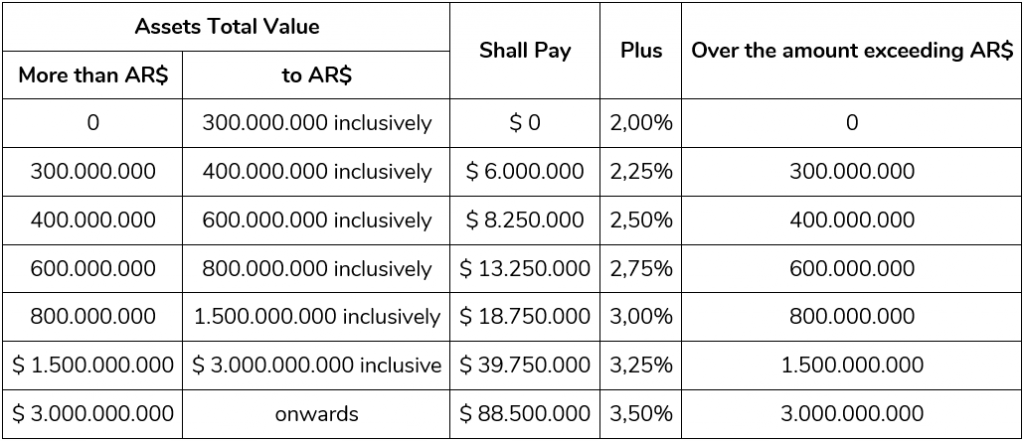

The payable contributions shall be the one calculated over the value of all the assets, in line with the following scale:

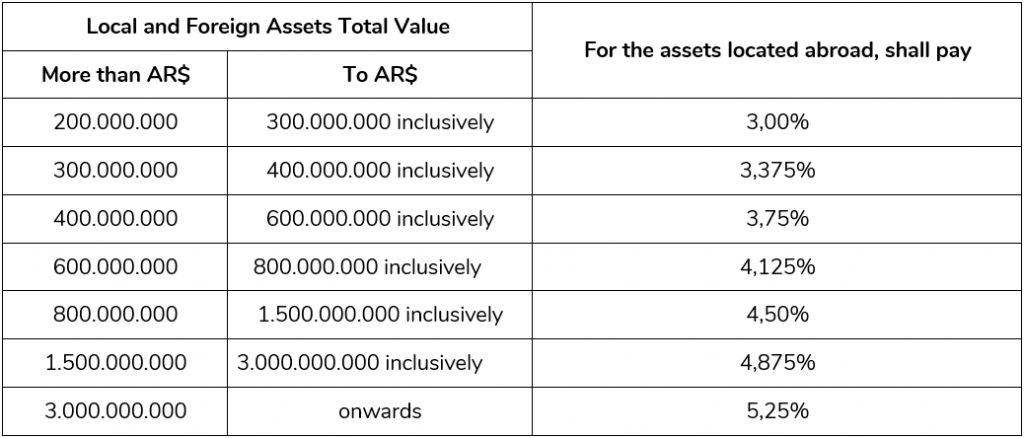

For assets located abroad, and in case no repatriation is verified, the Contribution shall be:

For the abovementioned purposes, repatriation means entry into the country within 60-days – extendable by the Executive Branch -, inclusively, as of the commencement validity date of this Law of: (i) foreign currency held abroad and (ii) the amounts arising from the realization or disposal of financial assets abroad – in terms of article 25 of the Wealth Tax Law -, that represent at least 30% of the total value of such assets. Upon repatriation, funds must remain in an open bank account until December 31st, 2020, or affected to one of the destinations to be established by the National Executive Branch.

The Law specifies that in case that the variation related to the taxable assets occurred during the next 180 immediate days prior to the commencement validity date of this Law support the presumption that is an evasive or stunt maneuver or is aimed at avoiding the payment of this contribution, the National Tax Authorities may stipulate to have them considered for purposes of determining the applicable Contribution.

This new Extraordinary and Mandatory Contribution may raise questions since its taxable event overlaps the Wealth Tax one, and thus being subject to internal double taxation. Moreover, the valuation rules and other specifications applicable to these Contributions are strictly the ones of the Wealth Tax Law.

{kind=link}

{kind=link}

{kind=link}